Simulation of the 3/2 model using the Quadratic exponential scheme#

In order to achieve maximum performance of Pytorch in a Monte-Carlo simulation it is critical to vectorize over the number of simulations. Thus we need to remove all ‘if’ statements from the Quadratic Exponential scheme. Here we are also comparing the numerical performance with a standard Milstein-Euler scheme

[10]:

#import torch

import numpy as np

from quant_analytics_torch.analytics import blackanalytics

from icecream import ic

from quant_analytics_torch.calculators.multivariatebrownianbridge import MultivariateBrownianBridge

from quant_analytics_torch.analytics.norminv import norminv

import matplotlib

from matplotlib import pyplot as plt

from quant_analytics_torch.analytics import maxsoft

from quant_analytics_torch.analytics.characteristicfunction import heston_option_price, threeovertwo_option_price

[11]:

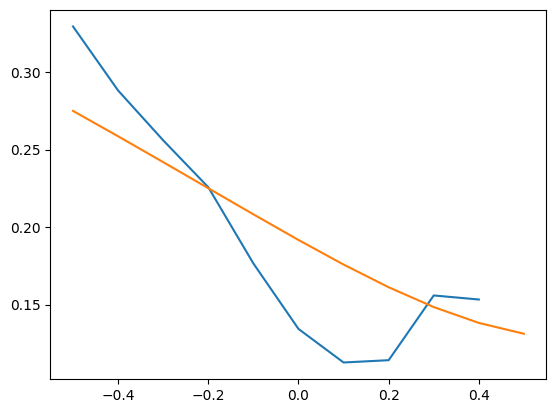

strikes = [-0.5, -0.4, -0.3, -0.2, -0.1, 0, 0.1, 0.2, 0.3, 0.4, 0.5]

ivs_heston = []

ivs_3_2 = []

for it in strikes:

strike = np.exp(it)

price = heston_option_price(strike,1,0.04,1,0.04,1,-0.7,1)

iv = blackanalytics.impliedvolatility(price,1,strike,1)

ivs_heston.append(iv)

for it in strikes:

strike = np.exp(it)

price = threeovertwo_option_price(strike,1,0.04,22,0.09,8,-0.8,1)

iv = blackanalytics.impliedvolatility(price.real,1,strike,1)

ivs_3_2.append(iv)

print(ivs_heston)

print(ivs_3_2)

[0.329324589130455, 0.28804817090987134, 0.2559429643335339, 0.22570594900838947, 0.1765775635550539, 0.13437616926929888, 0.11274163089679885, 0.11420776457099098, 0.15594420454274932, 0.1533360730988036, inf]

[0.27490070281895745, 0.2585383473876623, 0.24188987704203105, 0.22506545950438872, 0.208247085020842, 0.19171477686187532, 0.17586904342594117, 0.16123827628813256, 0.14846157304813323, 0.13824363532984824, 0.13125438320876792]

[9]:

plt.plot(strikes,ivs_heston)

plt.plot(strikes,ivs_3_2)

[9]:

[<matplotlib.lines.Line2D at 0x7fe263369e90>]

[2]:

def milstein_euler_simulation(rho, theta, kappa, eta, T, paths, n_dt):

dt = T/n_dt

dim = n_dt

sobol_engine = torch.quasirandom.SobolEngine(2*dim)

x = sobol_engine.draw(1)

u = sobol_engine.draw(paths,dtype=torch.float64)

states = 2

dim = n_dt

fm = torch.zeros(size=(states,states))

fm[0][0] = 1.

fm[0][1] = 0.

fm[1][0] = 0.

fm[1][1] = 1.

fwd_cov = torch.zeros(size=(dim, states, states))

for i in range(dim):

fwd_cov[i] = fm

multivariate_brownian = MultivariateBrownianBridge(fwd_cov)

y = norminv(u)

y = torch.reshape(y, shape=(dim,states,paths))

dz = multivariate_brownian.path(y, True)

X = torch.zeros([paths])

V = torch.zeros([n_dt+1,paths])

Vt = torch.zeros([paths])

Vt[:] = theta

V[0] = theta

for i in range(n_dt):

z2 = dz[i][1]

z1 = dz[i][0]

Vt = torch.maximum((Vt + kappa*theta*dt + eta*torch.sqrt(Vt*dt)*z2+0.25*eta*eta*dt*(z2*z2-1.))/(1+kappa*dt),torch.tensor(0.))

X = X - V[i]*dt/2 + torch.sqrt(V[i]*dt)*(rho*z2 + torch.sqrt(1-rho*rho)*z1)

V[i+1] = Vt

return X

[3]:

def quadratic_exponential(rho, theta, kappa, eta, T, paths, n_dt):

dt = T/n_dt

dim = n_dt

gamma1 = 0.5

gamma2 = 0.5

K0 = -(rho*kappa*theta)*dt/eta

K1 = gamma1*dt*(-0.5+(kappa*rho/eta))-(rho/eta)

K2 = gamma2*dt*(-0.5+(kappa*rho/eta))+(rho/eta)

K3 = gamma1*dt*(1-rho**2)

K4 = gamma2*dt*(1-rho**2)

sobol_engine = torch.quasirandom.SobolEngine(2*dim)

x = sobol_engine.draw(1)

u = sobol_engine.draw(paths,dtype=torch.float64)

u = torch.transpose(u,0,1)

# Random variable for the underlying

u1 = u[:dim]

# Random variables for the volatility

u2 = u[dim:]

states = 1

dim = n_dt

fm = torch.zeros(size=(states,states))

fm[0][0] = 1.

fwd_cov = torch.zeros(size=(dim, states, states))

for i in range(dim):

fwd_cov[i] = fm

multivariate_brownian = MultivariateBrownianBridge(fwd_cov)

y = norminv(u1)

y = torch.reshape(y, shape=(dim,states,paths))

dz = multivariate_brownian.path(y, True)

X = torch.zeros([paths])

V = torch.zeros([n_dt+1,paths])

Vt = torch.zeros([paths])

Vt[:] = theta

V[0] = theta

for i in range(n_dt):

minusexpkappadt = torch.exp(-kappa*dt)

m = theta+( Vt - theta) * minusexpkappadt

s2 = ((Vt*eta**2) * minusexpkappadt/kappa)*(1-minusexpkappadt) + ( theta*eta**2)*((1-minusexpkappadt)**2)/(2*kappa)

phi = s2/m**2

#

# Calculate the lower branch

#

psi_2 = 2/phi

b2 = torch.maximum(psi_2-1+(torch.sqrt(psi_2))*(torch.sqrt(torch.maximum(psi_2-1, torch.tensor(0.)))),torch.tensor(0.))

a = m/(1+b2)

z2 = norminv(u2[i])

Vnew_1 = a*(z2 + torch.sqrt(b2))**2

#

# Calulcate the upper branch

#

p = (phi-1)/(phi+1)

beta = (1-p)/m

Vnew_2 = torch.log((1-p)/(1-u2[i])) / beta

Vnew_2 = torch.maximum(Vnew_2, torch.tensor(0.))

phiC = 1.5

#

# Switch the branches

#

p_1 = maxsoft.soft_heavy_side_hyperbolic(phiC-phi, 0.00001)

q_1 = 1. - p_1

Vt = p_1 * Vnew_1 + q_1 * Vnew_2

V[i+1] = Vt

#

# Update the underlying

#

#z1 = norminv(u1[i])

z1 = dz[i][0]

X = X + K0 + K1*V[i] + K2*Vt + (torch.sqrt(K3*V[i]+K4*Vt))*z1

return X

[4]:

rho = torch.tensor(-0.27829, requires_grad=True)

theta = torch.tensor((0.3095)**2, requires_grad=True)

kappa = torch.tensor(1., requires_grad=True)

eta= torch.tensor(0.9288, requires_grad=True)

T = 1

paths =2**14-1

n_dt = 64

[5]:

X_milstein = milstein_euler_simulation(rho, theta, kappa, eta, T, paths, n_dt)

[6]:

X_qe = quadratic_exponential(rho, theta, kappa, eta, T, paths, n_dt)

[8]:

Sm = torch.exp(X_milstein)

Sq = torch.exp(X_qe)

Savg = torch.mean(Sm)

Pavg = torch.mean(torch.maximum(Sm-1.,torch.tensor(0.)))

print(Savg)

print(Pavg)

tensor(0.9971, grad_fn=<MeanBackward0>)

tensor(0.1043, grad_fn=<MeanBackward0>)

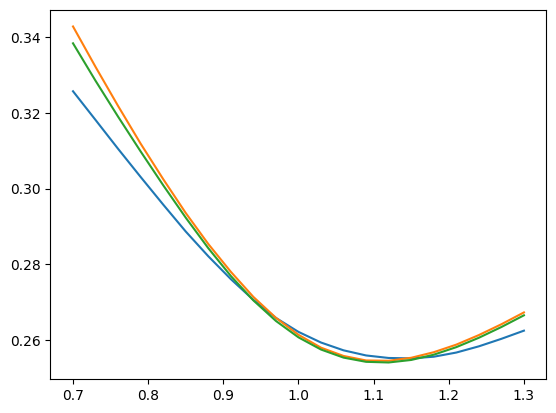

[11]:

nk = 21

k = np.linspace(0.7,1.3,nk)

ivm = torch.zeros(nk)

ivq = torch.zeros(nk)

ivh = torch.zeros(nk)

for it,ik in enumerate(k):

pm = torch.mean(torch.maximum(Sm-ik,torch.tensor(0.))).detach().numpy()

ivm[it] = blackanalytics.impliedvolatility(pm, 1., ik, T)

pq = torch.mean(torch.maximum(Sq-ik,torch.tensor(0.))).detach().numpy()

ivq[it] = blackanalytics.impliedvolatility(pq, 1., ik, T)

ph = heston_option_price(ik, 1., theta.detach().numpy(), kappa.detach().numpy(), theta.detach().numpy(), eta.detach().numpy(), rho.detach().numpy(), T)

ivh[it] = blackanalytics.impliedvolatility(ph, 1., ik, T)

/home/vscode/.local/lib/python3.11/site-packages/scipy/integrate/_quadpack_py.py:575: ComplexWarning: Casting complex values to real discards the imaginary part

return _quadpack._qagse(func,a,b,args,full_output,epsabs,epsrel,limit)

[12]:

plt.plot(k,ivm)

plt.plot(k,ivq)

plt.plot(k,ivh)

[12]:

[<matplotlib.lines.Line2D at 0x7f7483548d50>]